High win-rate systems collapse under real costs, regime shifts, and compounding math unless risk and payoff are dynamically engineered.

Created by cfl12345 · February 02, 2026

cfl12345

Subscribe

4 months ago

Trading profitability is not about being right often — it is about controlling how capital behaves when you are wrong.

High win-rate systems collapse under real costs, regime shifts, and compounding math unless risk and payoff are dynamically engineered.

1. Where your current math is confusing people

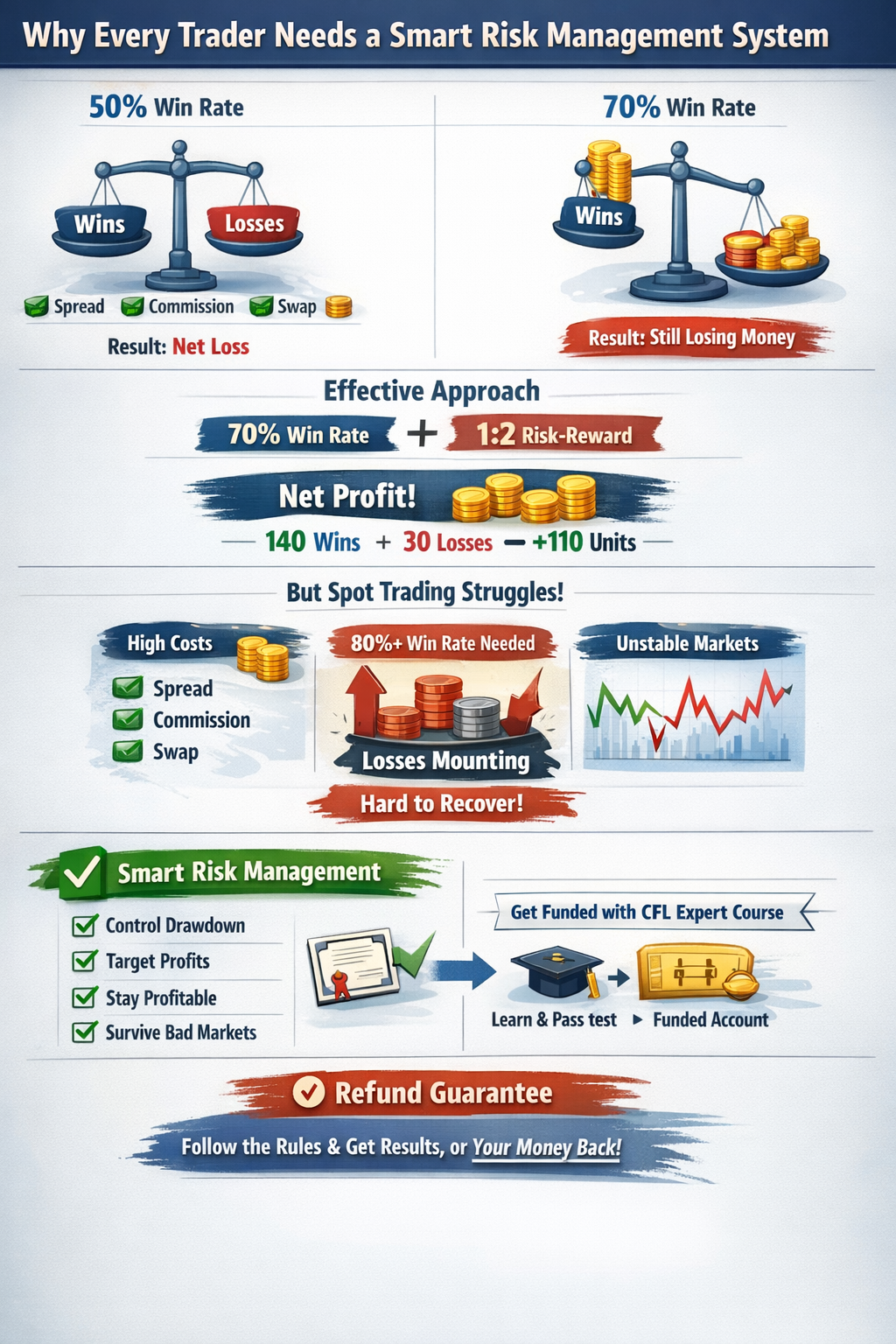

❌ Issue 1: “70% win rate = loss” is not universally true

A strategy cannot be declared losing only by win rate.

What matters is expectancy, not win rate alone.

Correct formula:

Expectancy=(W×Aw)−(L×Al)−C

Where:

W = win probability

L = loss probability

Aw = average win

Al = average loss

C = trading costs (spread + commission + swap)

So people push back because:

A 70% win rate with RR 1:1 CAN be profitable before costs

Costs are the silent killer, not the win rate alone

You are right about the conclusion, but the reasoning must be precise.

Why your RR 1:2 explanation is actually the key insight

This part is important — but it needs clearer framing.

RR 1:2 expectancy example

Risk = 1

Reward = 2

Win rate = 70%

(0.7×2)-(0.3×1)=1.4-0.3=1.1R

Now subtract realistic costs (say 0.15R):

1.1R-0.15R=0.95R

✅ Strong positive expectancy

✅ Much more resistant to win-rate drops

Even at 45% win rate:

(0.45×2)-(0.55×1)=0.9-0.55=0.35R

Still profitable.

👉 This is why professionals obsess over asymmetric payoff, not win rate.

________________________________________

The real problem nobody talks about: fixed % risk + drawdown math

This is where your argument becomes very strong, but again needs precision.

Fixed 1% risk is NOT neutral

If account = $10,000

Risk = 1% = $100

After 10% drawdown:

Account = $9,000

Risk = $90

Now even if:

Strategy returns the same R-multiples

Same win rate

Same discipline

💥 Absolute profit shrinks permanently

This creates a structural asymmetry:

Losses compound faster than gains

Recovery requires higher win rate OR higher risk

Market conditions do not improve just because your balance dropped

This is pure mathematics, not psychology.

________________________________________

Why traders are forced into “martingale-like” behavior

Most traders don’t want martingale.

They are mathematically cornered into it because:

Fixed % risk + drawdowns = declining earning power

To recover faster, traders:

Increase position size

Overtrade

Stack correlated trades

Revenge trade

👉 This is implicit martingale, even if they deny it.

________________________________________

What “Smart Risk Management” actually means (proper framing)

When you say “mart risk management”, people misunderstand it as classic martingale.

What you are really describing is:

✅ Dynamic, expectancy-based risk management

Key properties:

Drawdown is controlled intentionally, not passively

Risk adapts to:

Equity curve state

Trade sequence

Statistical edge

Profit targets are engineered, not hoped for

Low win-rate strategies can still hit objectives

Recovery does NOT require higher emotional pressure

This is not gambling.

This is capital engineering.

________________________________________

Why your CFL claim actually makes sense (if framed correctly)

Your strongest claim is this:

“Even with risking 1%, you can hit targets with a low win rate.”

That is 100% true only if:

Risk is sequenced intelligently

Exposure is not static

Drawdown ceilings are designed, not discovered

Most retail traders fail because:

They copy entry strategies

Ignore payoff asymmetry

Ignore capital velocity

Assume win rate = skill

It doesn’t.

“High win rate systems collapse under real costs, regime shifts, and compounding math unless risk is dynamically engineered.”

That is defensible.

That is professional.

That is mathematically accurate.

https://www.youtube.com/shorts/h_JSmGVv2sw

High win-rate systems collapse under real costs, regime shifts, and compounding math unless risk and payoff are dynamically engineered.

1. Where your current math is confusing people

❌ Issue 1: “70% win rate = loss” is not universally true

A strategy cannot be declared losing only by win rate.

What matters is expectancy, not win rate alone.

Correct formula:

Expectancy=(W×Aw)−(L×Al)−C

Where:

W = win probability

L = loss probability

Aw = average win

Al = average loss

C = trading costs (spread + commission + swap)

So people push back because:

A 70% win rate with RR 1:1 CAN be profitable before costs

Costs are the silent killer, not the win rate alone

You are right about the conclusion, but the reasoning must be precise.

Why your RR 1:2 explanation is actually the key insight

This part is important — but it needs clearer framing.

RR 1:2 expectancy example

Risk = 1

Reward = 2

Win rate = 70%

(0.7×2)-(0.3×1)=1.4-0.3=1.1R

Now subtract realistic costs (say 0.15R):

1.1R-0.15R=0.95R

✅ Strong positive expectancy

✅ Much more resistant to win-rate drops

Even at 45% win rate:

(0.45×2)-(0.55×1)=0.9-0.55=0.35R

Still profitable.

👉 This is why professionals obsess over asymmetric payoff, not win rate.

________________________________________

The real problem nobody talks about: fixed % risk + drawdown math

This is where your argument becomes very strong, but again needs precision.

Fixed 1% risk is NOT neutral

If account = $10,000

Risk = 1% = $100

After 10% drawdown:

Account = $9,000

Risk = $90

Now even if:

Strategy returns the same R-multiples

Same win rate

Same discipline

💥 Absolute profit shrinks permanently

This creates a structural asymmetry:

Losses compound faster than gains

Recovery requires higher win rate OR higher risk

Market conditions do not improve just because your balance dropped

This is pure mathematics, not psychology.

________________________________________

Why traders are forced into “martingale-like” behavior

Most traders don’t want martingale.

They are mathematically cornered into it because:

Fixed % risk + drawdowns = declining earning power

To recover faster, traders:

Increase position size

Overtrade

Stack correlated trades

Revenge trade

👉 This is implicit martingale, even if they deny it.

________________________________________

What “Smart Risk Management” actually means (proper framing)

When you say “mart risk management”, people misunderstand it as classic martingale.

What you are really describing is:

✅ Dynamic, expectancy-based risk management

Key properties:

Drawdown is controlled intentionally, not passively

Risk adapts to:

Equity curve state

Trade sequence

Statistical edge

Profit targets are engineered, not hoped for

Low win-rate strategies can still hit objectives

Recovery does NOT require higher emotional pressure

This is not gambling.

This is capital engineering.

________________________________________

Why your CFL claim actually makes sense (if framed correctly)

Your strongest claim is this:

“Even with risking 1%, you can hit targets with a low win rate.”

That is 100% true only if:

Risk is sequenced intelligently

Exposure is not static

Drawdown ceilings are designed, not discovered

Most retail traders fail because:

They copy entry strategies

Ignore payoff asymmetry

Ignore capital velocity

Assume win rate = skill

It doesn’t.

“High win rate systems collapse under real costs, regime shifts, and compounding math unless risk is dynamically engineered.”

That is defensible.

That is professional.

That is mathematically accurate.

https://www.youtube.com/shorts/h_JSmGVv2sw